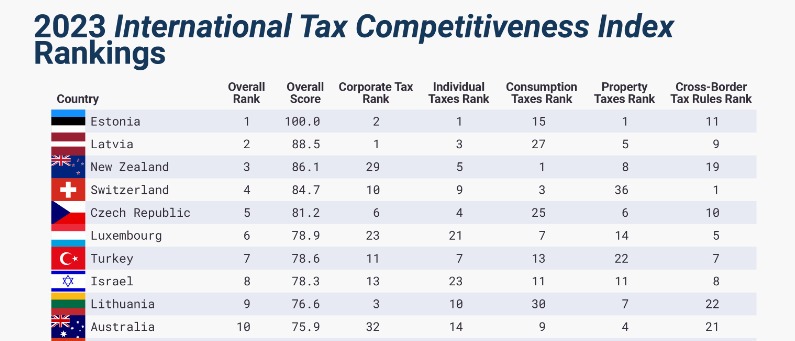

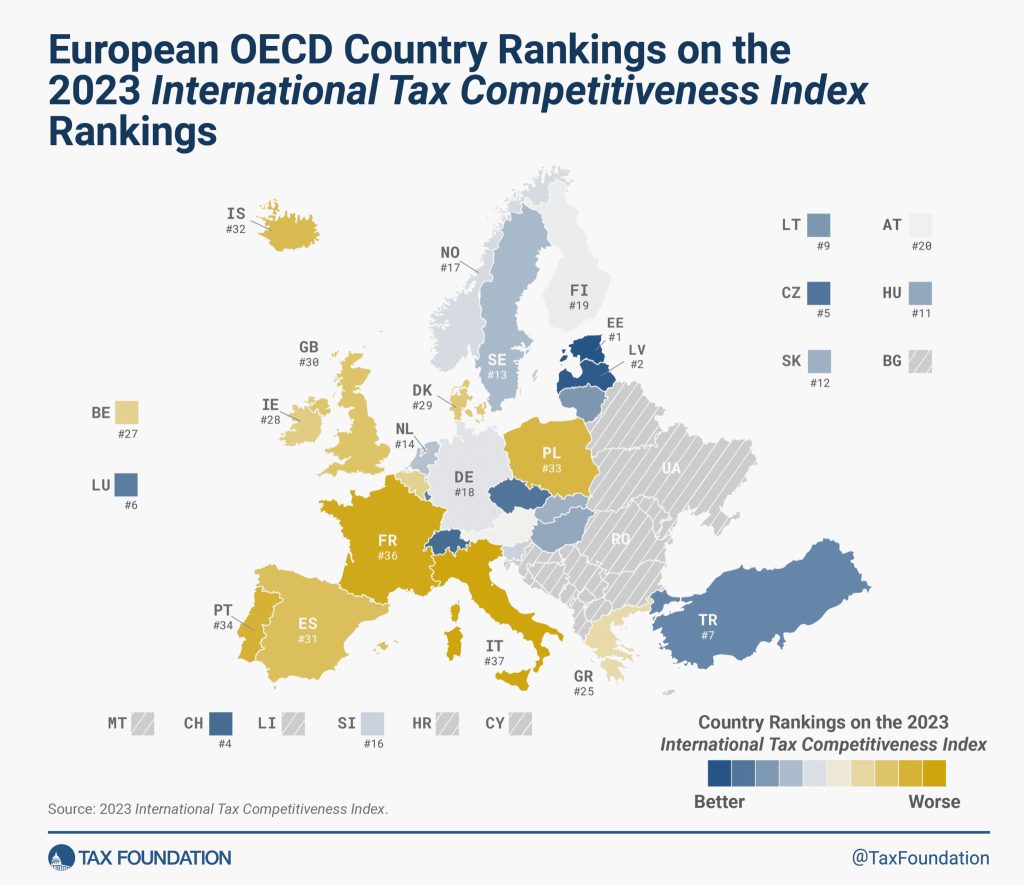

estonia’s tax system most competitive in the world

Looking forward to 2024-26 and changes to Estonian taxes

From 1 January 2024:

From 1 January 2025:

Security tax package

More from e-Residency

- Sign up for our newsletter

- Watch fresh video content - subscribe to our Youtube channel

- Meet our team and e-residents - register for our next Live Q&A

Read next

Moving toward cardless e-Residency with biometric mobile app

Interesting e-resident stats to celebrate our 11th anniversary

Estonia invites South African entrepreneurs to join its digital nation through e‑Residency

Study trip: Global founders explore the Estonian startup ecosystem